Just in time for the 100th anniversary of the foundation of the Chinese Communist Party in July, Chinese equities are bouncing back, with Industrial China clearly the biggest beneficiary of the post-Covid-19 reopening of the US and European economies. Technically speaking, the fact that Chinese equities distanced themselves tangibly from critical support levels should avoid a decoupling of this market.

China was First In – First Out of the Covid-19 pandemic and the economy posted 2.3% of GDP growth last year - the only major economy to report an expansion in 2020. Even though its stock market reacted accordingly, it underperformed in the first months of 2021. This year, stocks geared to the reopening have bounced back, first in the US and now in Europe. In continental Europe, the vaccine rollout and the subsequent reopening have been delayed, leaving some catch-up potential. One should, however, not forget that the reopening in the Western world is a new positive factor for the Chinese economy.

A positive feedback loop is developing here, leaving industrial China a winner. The recent uptick in China’s manufacturing Caixin PMI to a new high for 2021 reflects both the global recovery and ongoing domestic demand. We expect both developments to continue, going by the rise in both the domestic and export orders components. Clearly, the recent recovery has been supported by significant monetary and fiscal accommodation in the Western world and, of course, vaccine success. Chinese exporters, still the prime global supplier in many areas of the industrial sector, are producing to fill surging post-Covid orders.

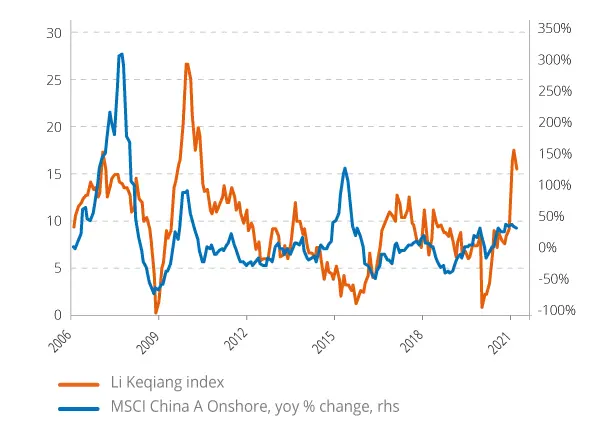

We use the so-called Li Keqiang index (named after the current Chinese Prime minister) to monitor economic output in China. A composite indicator based on freight volume, electricity consumption and total loans, this gauge has just hit its highest level since 2010. The ongoing strength of the Chinese economy is supportive of its stock market. In particular, we are maintaining our positive view on the supply chain rebuild and infrastructure (both traditional and green infrastructure) in the industrial sector.

Strong Chinese economic recovery supportive of domestic Chinese equities

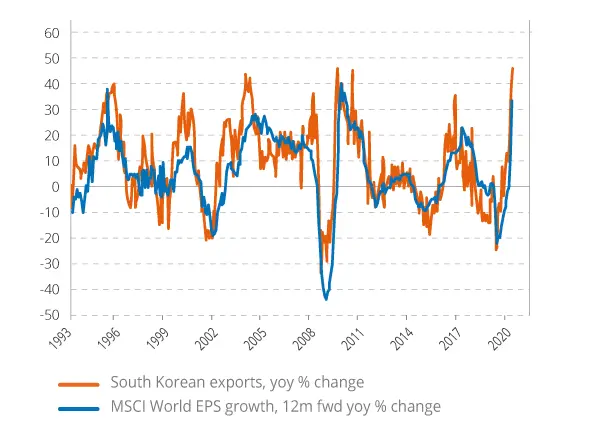

We already noted the unique bullish macroeconomic environment earlier this year. Beyond China, two other factors are retaining our attention: first, commodity-price strength. Contrary to conventional wisdom, this evolution is lifting industrial profits in China as extra raw material costs are passed on, including to overseas customers. Second, the surge in South Korea’s exports. Strength in overseas sales was broad-based, with 14 out of 15 major product categories posting increases during the month of May. While we like the combination of quality value (Financials) and growth (e.g. Technology and Healthcare) in South Korea specifically, we draw a more general positive conclusion from the recent numbers. South Korean exports have been an important leading indicator of the global profit cycle for the past three decades. The recent sharp recovery implies further upward earnings revisions from here, as the re-opening in the West and the industrial strength of Asia are a powerful mix.

South Korean exports: a good leading indicator of the global profit cycle